Financial House Keeping

/

Financial Housekeeping

Consider doing these key financial task headed into the new year

As we wrap up the year these are excellent financial housekeeping tips.

1. Consider Maxing out IRA Contributions:

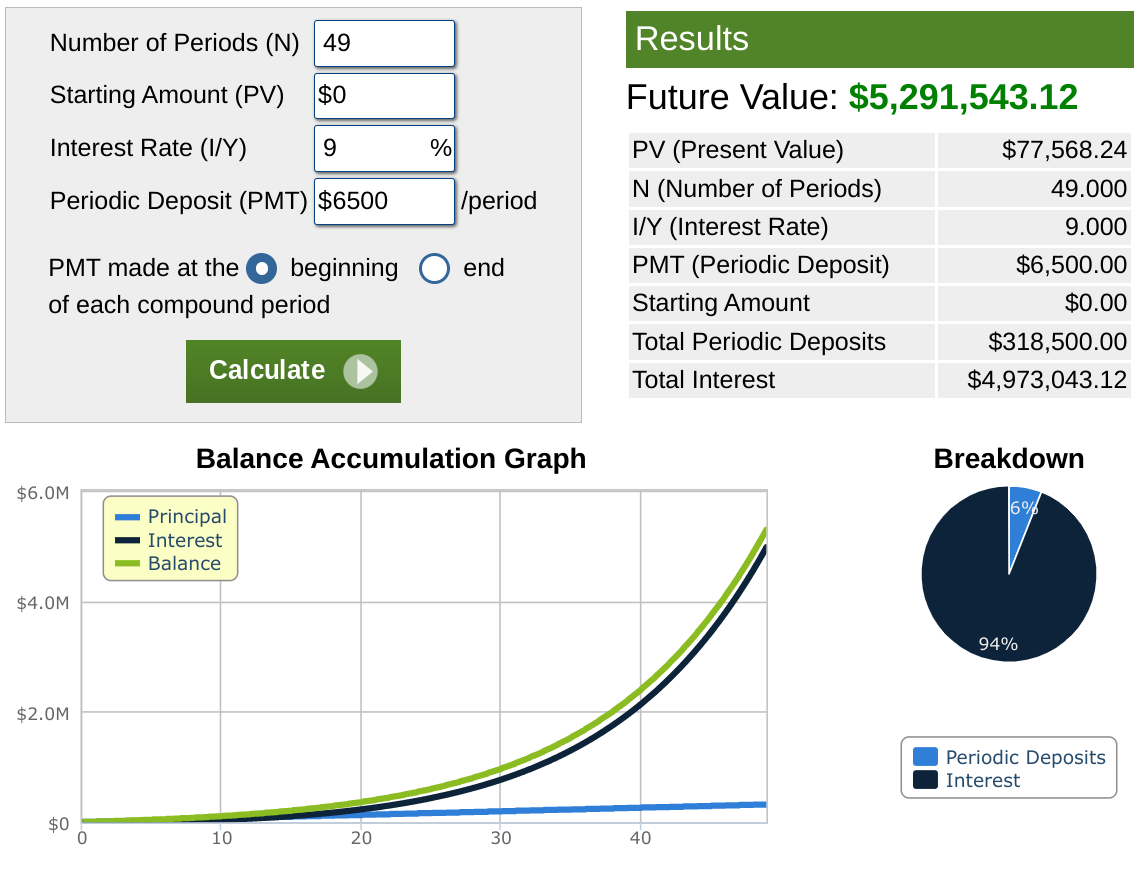

For those under 50, the allowable annual contribution to a traditional or Roth IRA is $6,500; for those 50 and older, it's $7,500. Evaluate the advantages of a pre-tax traditional IRA versus a Roth IRA in the context of your financial goals. Also, note the extended contribution deadline until April 15th, 2024, for the 2023 tax year.

2. Collecting Tax Documents:

As the year concludes, proactively compile a comprehensive list of all financial accounts. Anticipate incoming tax forms from relevant institutions. Timely receipt of these documents is imperative for accurate tax filing. Exercise diligence, recognizing that the responsibility for completeness lies with you.

3. Increase your 401k/403b Contributions:

Embrace the wisdom of Albert Einstein by incrementally enhancing contributions to your employer-sponsored retirement accounts. Recognize the intrinsic value of compound interest in wealth accumulation. Additionally, reassess your investment strategy to align with your financial objectives.

4. Update Beneficiaries:

Talking about wills might feel morbid, but it's like an insurance policy for your family's peace of mind. Keep your beneficiary info updated; life happens.

5. Maxing Out HSA Contributions:

HSAs are like secret savings accounts. Max them out if you can. And if you've got a flexible spending account (FSA), use that leftover cash; it doesn't roll over.

6. RMD’s:

If you're enjoying retirement and hitting 73 or older, remember to take out your required minimum distributions (RMDs). Missing it means penalties, big penalties. You have until December 31st to complete RMDs for 2023.

7. Updating Insurance:

Time to check your home and auto insurance. With things going up, make sure your coverage is on point. Get a free quote and consider bundling home and auto insurance for potential discounts.

8. Paying Off Debt:

Got some extra cash from holiday bonuses? Think about wiping out some debt. It's like giving yourself a head start for 2024. Less debt, less stress. Cheers to financial freedom!

9. Goal Setting:

Plan out your money goals for 2024 and beyond and jot them down. Seriously, you're 10 times more likely to make things happen when you put them on paper.

These are just a few friendly suggestions. Your money, your rules. But a bit of financial TLC can make a world of difference.

Sincerely,

Spencer Miller

12/21/2023